Everything You Need to Know About Motor Vehicle Dealer Bonds

Motor vehicle dealer surety bonds provide protection for customers, creditors, and governments.

Trust between all parties is essential for a motor vehicle dealer. Customers trust that the dealer has told them the truth about the vehicle that they'll use to drive their families around. Sellers and creditors trust that the dealer will pay them back for inventory and financing. State governments trust that dealers will abide by state laws and pay all required taxes. To grow and prosper, a motor vehicle dealer has to earn this trust by ensuring that all relevant third parties are protected in the event of a dispute or violation.

Motor vehicle dealer surety bonds provide protection for customers, creditors, and governments. In fact, most state governments require dealerships to obtain motor vehicle dealer bonds before the state will issue a dealership license. A motor vehicle dealer bond (also called an MVD bond, auto dealer bond, car dealer bond, or DMV bond) uses a third-party guarantor to provide a financial guarantee that an auto dealer will operate in compliance with legal and ethical standards.

An automobile dealer who needs to obtain a motor vehicle dealer surety bond should know the key facts about these bonds before starting their search. Here we'll cover the basics of how a motor vehicle dealer bond protects a dealer's customers and other important third parties. Then, we'll look at some of the most important types of vehicle dealer bonds and state laws regulating them. Finally, we'll learn about how dealer bonds are priced, and how you can get one.

How Does a Motor Vehicle Dealer Bond Work?

Watch our video explaining what an auto dealer bond is, when it's required, and why it's required.

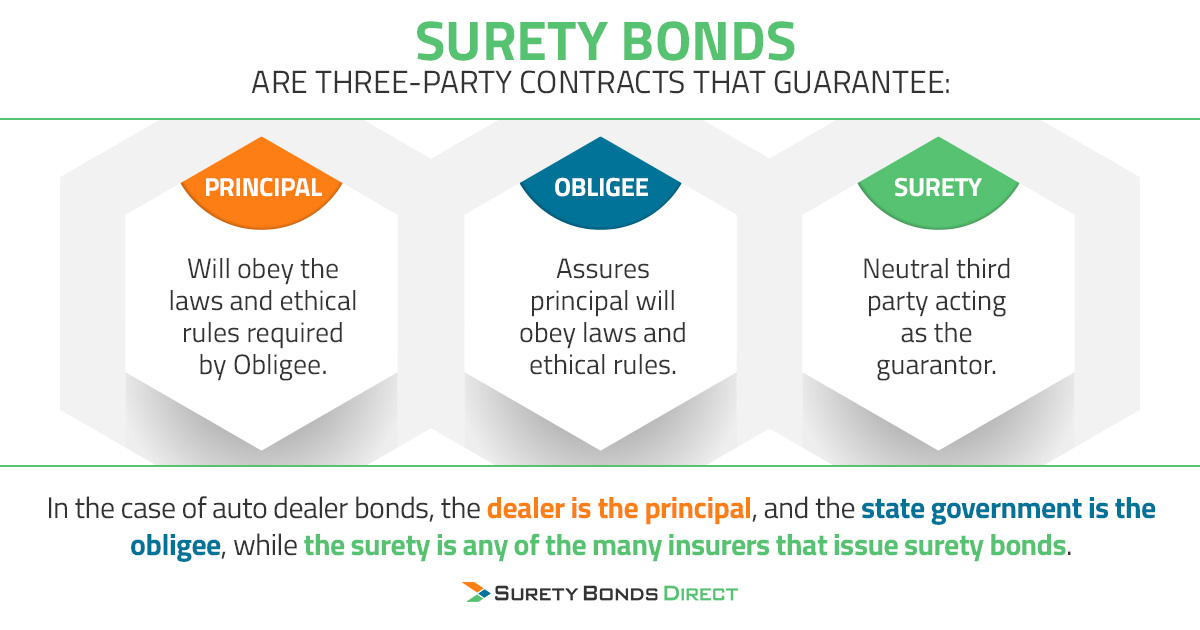

A motor vehicle dealer bond is a type of surety bond. Surety bonds are three-party contracts guaranteeing that one party (called the principal) will obey the laws and ethical rules required by another party (called the obligee), with a neutral third party (called the surety) acting as a guarantor.

In the case of auto dealer bonds, the dealer is the principal, and the state government (usually the Department of Motor Vehicles or the Secretary of State) is the obligee, while the surety is any of the many insurers that issue surety bonds. Unlike other types of insurance that a dealer might carry, a surety bond protects third parties such as customers and creditors rather than the dealer. If a third party believes that a vehicle dealer has failed to act legally and ethically, that party can file a claim with the surety that issued the dealer's bond.

The parties who can typically file a claim under a dealer bond include:

- Consumers who buy a vehicle from the dealer

- Sellers who sell a vehicle to the dealer

- Lenders who provide consumer financing through the dealer

- Creditors who finance the dealer's inventory

- State regulators who issue the dealership's license

Common reasons for which a third party can file a claim include:

- Misrepresentation of a vehicle's condition, including tampering with the odometer

- Failure to deliver a valid title certificate for a purchased vehicle

- Failure to pay the state government the required vehicle sales tax

- Selling stolen vehicles

- Failure to report a vehicle's sale

Most states offer searchable online databases of licensed dealers so that anyone can verify that a dealer is licensed and bonded before they visit the lot or buy a vehicle.

Types of Motor Vehicle Dealership and Which Bonds They Need

The best starting point for researching which kind of dealer bonds a dealership needs is to determine which type of dealership it is, and then look up the individual state's specific bond laws. Each of the many types of motor vehicle dealership can require its own types of surety bond, depending on what state it operates in:

- Franchise Dealership: These dealerships sell mainly or exclusively new vehicles through a franchise agreement with a vehicle manufacturer, although the dealership may also sell some used vehicles. For some states' surety bonds, such as Tennessee dealer bonds and Indiana dealer bonds, a single type of bond covers both franchised new car dealers and used vehicle retail dealers. In other states, such as Texas, franchised new car dealerships do not require MVD bonds at all.

- Independent Used Vehicle Dealership: Independent used dealerships sell used cars of a variety of makes. In almost all states independent used vehicle dealerships must have auto dealer surety bond, such as a Louisiana used motor vehicle dealer bond.

- Wholesale Dealership: Wholesale dealerships sell used cars in volume to other dealers. In most states, wholesale dealerships can use the same type of surety bond as retail used car dealers, but some require a separate bond, such as a California wholesale dealer bond.

- Wholesale Motor Vehicle Auction: Wholesale auction dealerships sell used cars at auction, typically to other dealers (although some are open to the public). Some states require a separate bond for auction dealers, such as a Colorado wholesale vehicle auction bond.

- Salvage Dealership: These dealerships specialize in dismantling non-functional vehicles and selling them for parts. A few states require special automotive dismantler or parts recycler bonds, such as Georgia, Alabama, and Arizona.

- Trailer/Motorsports/RV Dealership: Many dealerships sell other types of vehicles, such as trailers, motorcycles, ATVs, and RVs. Some states include this under a general MVD bond, while others require separate bonds, such as a Florida recreational vehicle dealer bond or a New Mexico motorcycle dealer bond.

State Requirements for Vehicle Dealership Bonds

Each state has substantially different laws governing which type of surety bonds a vehicle dealer needs. Thus, for anyone interested in becoming a vehicle dealer, it's important to research the applicable laws in the individual state in which your dealership will operate. To check the laws for your state, see our page on Motor Vehicle Dealer Bonds and click on any state for a quick summary of applicable requirements.

To provide a better picture of the wide scope of surety bond laws that govern motor vehicle dealers, we've assembled a quick list of some oddities in the laws that many dealers miss or don't know about:

- New York dealer surety bond penalty requirements are based on the volume of vehicles that a dealer sells. 50 vehicles is the key number: dealers who sell more than 50 vehicles annually must obtain a $100,000 bond, while lower-volume dealers who sell fewer than 50 vehicles only need a $20,000 bond. New car dealers are required to obtain a $50,000 bond.

- Some states, such as Florida and Georgia, have fixed expiration dates for auto dealer bonds. Georgia motor vehicle dealer surety bonds expire on March 31st of even-numbered years, and auto-parts dealer surety bonds expire on December 31st of odd-numbered years. Florida motor vehicle dealer surety bonds expire on April 30th for independent dealer bonds, December 31st for franchise dealer bonds, and September 30th for recreational vehicle bonds. Texas motor vehicle dealer surety bonds, meanwhile, are issued for two-year terms and always expire on the last day of the month 2 years from the effective date, unless the bond was made effective on the 1st of the month, in which case the bond is valid for exactly 2 years.

- Many states include common dealership services, such as towing and repair service, within the scope of the bond. However, other states require separate bonds for these services, such as a Connecticut motor vehicle repairer bond.

- Although some states, such as California, require a dealer's sales associates to have vehicle sales licenses, individual salespeople do not need their own surety bonds to become licensed.

- In some states, a dealer bond is also referred to as a designated agent bond, which is why you'll see terms like "Illinois designated agent bond" and "Illinois designated agent bond" used occasionally.

- Although the typical motor vehicle dealer bond covers a one-year period, many sureties will offer bonds for two- or three-year terms as well.

How Much Does a Dealer Surety Bond Cost?

Two main factors determine the premiums a dealer will pay for an MVD surety bond:

- Bond Amount: Each state requires dealer bonds to cover a certain amount - often referred to as the "bond penalty." The premium (the amount you pay) is set as a percentage of the bond amount, typically one percent to three percent for a dealership with a good credit score. There are cases where the premium can be below 1 percent, especially for dealers with more years in business or a long history of being bonded without claims.

- Credit Score: Credit score is the most important factor in determining the premium a surety will charge a dealer to obtain a surety bond. Regardless of which surety bond is being issued, or in which state the bond is issued, a surety always wants to know that the principal has the financial capacity to repay any claims and that the principal will operate in a way that makes claims less likely in the first place. Thus, a principal with a credit score under 625 will typically pay a higher premium to obtain a surety bond than a principal with a score of over 625.

Note that Surety Bonds Direct can help you obtain a dealer bond even if you don't have great credit. For more information on how a credit score affects a business's surety bond premiums, as well as options for principals with lower credit scores, such as co-signers and premium financing, read our article on How to Get a Surety Bond with Bad Credit.

Obtaining an auto dealer surety bond is a requirement for most people opening a vehicle dealership, but it doesn't have to be a long or stressful process. Surety Bonds Direct works directly with A-rated sureties to get our customers the lowest premiums available on motor vehicle dealer bonds. For more information on our full range of dealer bonds, contact our bond specialists at 1-800-608-9950 or use our easy two-minute surety bond quote request to get your quote today.

updated: