Surety Bond vs. Letter of Credit: Everything You Need to Know

Surety bonds and letters of credit help create accountability between the various parties of a construction contract. They protect project owners, subcontractors, suppliers, and even contractors themselves from losses resulting from breaches of contract.

Any large construction project involves substantial obligations on a contractor's part. Project owners, material suppliers, and subcontractors must have the confidence that a contractor will pay debts and complete all work in full. Often, a contractor will be required to obtain legal and financial guarantees that they will fulfill their obligations.

That’s why surety bonds and letters of credit are a crucial part of the world of construction. Surety bonds and letters of credit are two different types of legal contracts that help establish trust and accountability for a contractor. Each uses a different mechanism to provide a financial guarantee that a contractor will meet their obligations to the many other stakeholders on a construction project.

Here, we’ll provide an overview of several key topics for construction contractors, including What Is a Surety Bond and What Is a Letter of Credit? Why are surety bonds and letters of credit important for construction contracts? What’s the difference between a surety bond vs. a letter of credit? Let’s begin our investigation with some basic definitions.

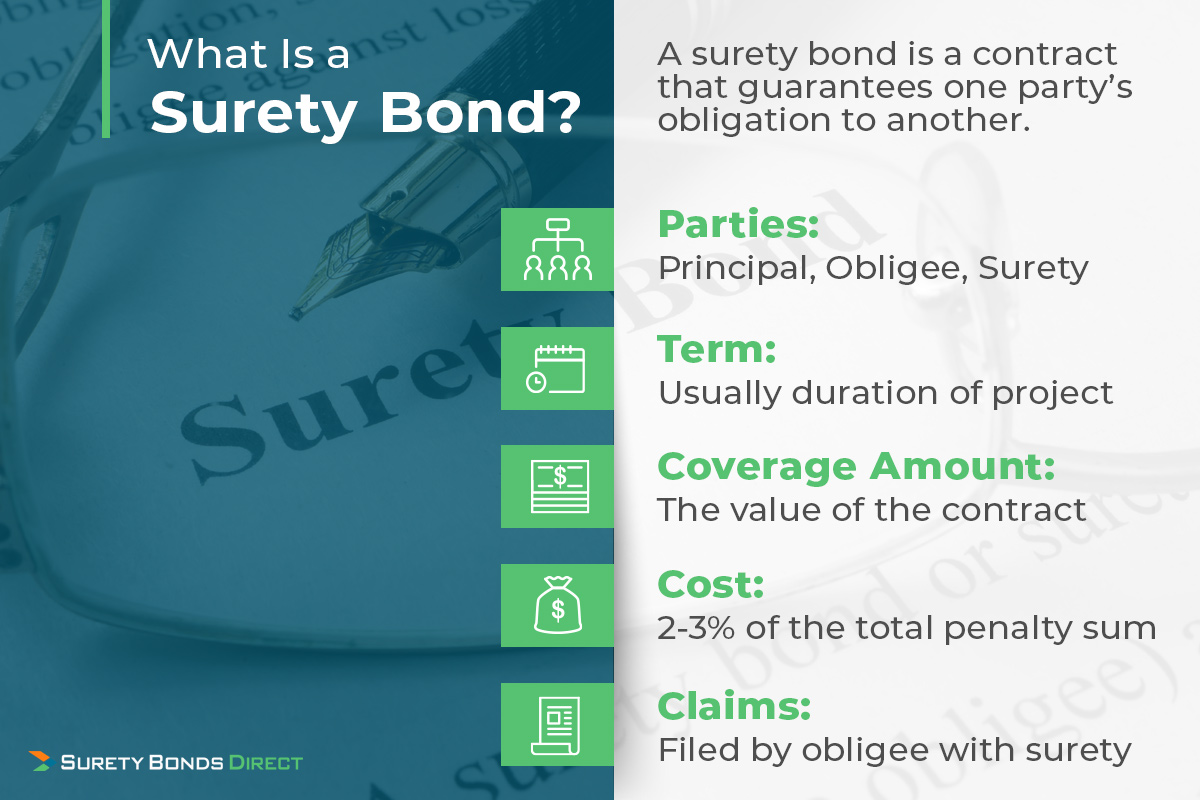

What Is a Surety Bond?

A surety bond is a three-party contract that guarantees one party’s obligation to another using an independent third party. In the case of a construction contract, the contractor purchases the bond at the request of the project owner, which might be either a private or government entity.

- Surety Bond Parties

-

- Principal: The party that purchases a surety bond to guarantee its obligation

- Obligee: The party that requires the principal to purchase the surety bond

- Surety: A neutral third party that guarantees the principal’s obligation up to a predetermined maximum called the penalty sum

- Bond Term

- Usually the duration of the project, sometimes with an additional period afterward known as the maintenance period during which the contractor is still liable for any defects in the work

- Coverage Amount

- The value of the contract, or an amount specified by the obligee

- Cost

- A premium equal to approximately 2 to 3 percent of the total penalty sum, depending on the principal’s credit score and financial history

- Claims

- Filed by the obligee with the surety; the surety will then investigate and pay out the claim if it’s factually and contractually valid

One more important thing to know about surety bonds is that the principal is fully liable for repaying any money that the surety pays to a claimant. Thus, the principal should always attempt to negotiate disputes with creditors and project owners before they escalate into a surety bond claim.

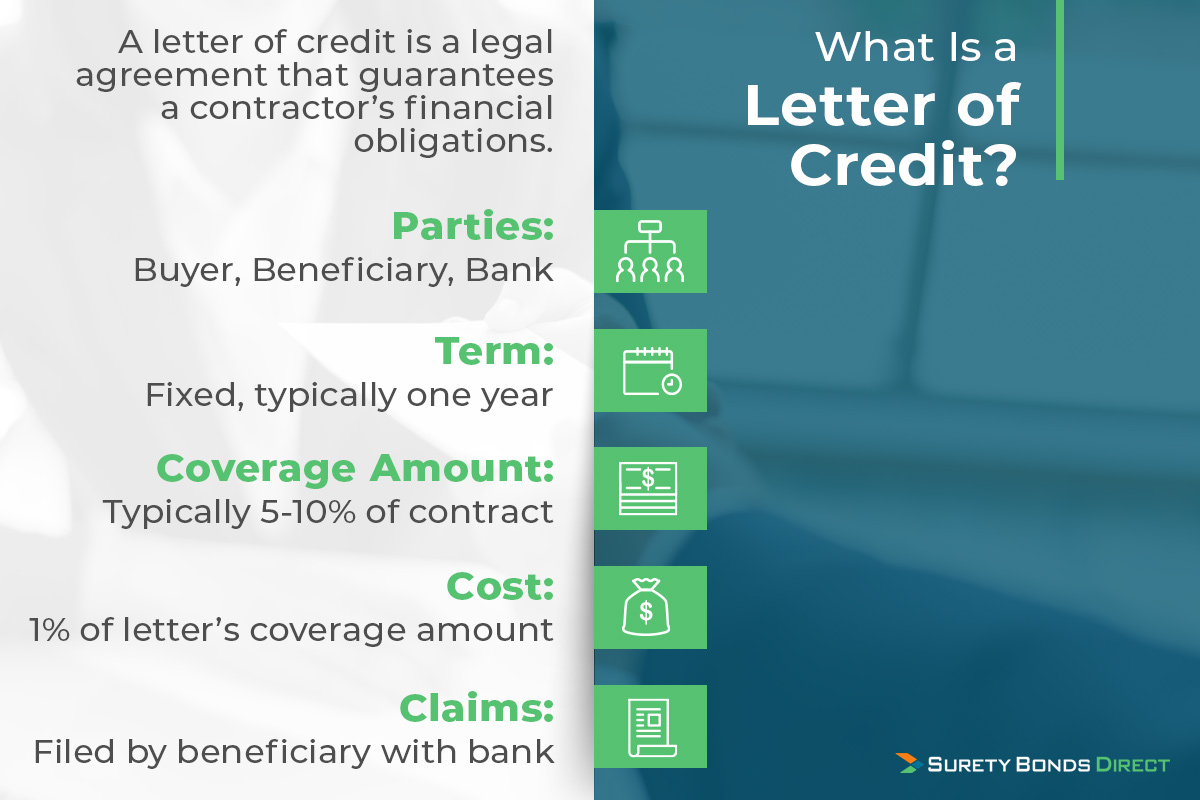

What Is a Letter of Credit?

A letter of credit is another type of legal agreement that creates a guarantee for a contractor’s financial obligations. Instead of a surety, a letter of credit uses a bank as the guarantor. Should the contractor fail to honor their obligations, the parties specified in the letter of credit can file a claim with the bank for financial reimbursement.

- Parties for a Letter of Credit

-

- Buyer: The party that purchases the letter of credit to guarantee its obligations

- Beneficiary: The party that is entitled to draw funds from the letter of credit if the buyer does not meet their obligations

- Bank: The financial institution that writes the letter of credit and holds the funds guaranteeing the obligation, up to a predetermined maximum

- Buyer

- The party that purchases the letter of credit to guarantee its obligations

- Beneficiary

- The party that is entitled to draw funds from the letter of credit if the buyer does not meet their obligations

- Bank

- The financial institution that writes the letter of credit and holds the funds guaranteeing the obligation, up to a predetermined maximum

- Term

- Fixed, typically one year, although some can be automatically renewed

- Coverage Amount

- Typically five to ten percent of the contract value, although in some cases, the letter of credit amount required may be higher. Such higher requirements may be required if the contractor has limited job history, prior surety bond claim payouts, a weak balance sheet or adverse personal and business credit.

- Cost

- Approximately one percent of the letter’s coverage amount paid as fees to the bank

- Claims

- Filed by the beneficiary with the bank, which will pay out the requested sum once it verifies that the beneficiary has followed any required procedures for filing a claim

A letter of credit is sometimes also called an irrevocable letter of credit because it can’t be canceled without the mutual agreement of all parties. The irrevocable status makes it a common choice for providing collateral backing to guarantee the terms of an agreement in a construction contract, as well as in some other areas such as international trade deals.

Why Surety Bonds and Letters of Credit Are Important

Surety bonds and letters of credit help create accountability between the various parties of a construction contract. They protect project owners, subcontractors, suppliers, and even contractors themselves from losses resulting from breaches of contract.

Fraud and breaches of contract are startlingly common in the construction industry and, without a surety bond or letter of credit, recovering damages from a breach of contract can be a long and complex process. Surety bonds and letters of credit ensure that creditors can use an orderly and legally valid process to recover damages within a reasonable time.

Before signing a contract, the parties must decide whether the contractor’s obligations will be backed by surety bonds or letters of credit. Next, we’ll compare these two options and learn about why surety bonds often come out on top in the matter of surety bonds vs. letters of credit.

Comparing a Surety Bond vs. Letter of Credit

Surety bonds and letters of credit are similar in many ways. Both are three-party agreements in which one party pays a neutral guarantor to provide a financial guarantee of an obligation. A contractor may have the choice between a surety bond and a letter of credit when signing the contract for a project.

However, there are several important differences between a surety bond and a letter of credit. These differences also help illustrate why a surety bond is often a better choice for contractors than a letter of credit.

- Sureties investigate claims made against a surety bond to verify that a breach of contract occurred. This helps defend the contractor against any potential fraudulent claims and makes it easier for the contractor or surety to challenge a claim in court. A letter of credit, on the other hand, gives the beneficiary the right to draw down funds at their discretion and offers the buyer relatively few resources for challenging a false claim.

- A surety bond has no negative effects on a contractor’s credit or borrowing capacity. Approval for a surety bond is based on a contractor’s financial solvency and credit history, but the bond does not appear on the contractor’s balance sheet. By contrast, a letter of credit does appear on a contractor’s balance sheet and may affect the contractor’s credit, much as other extensions of credit, such as a loan, might.

- Banks often impose additional terms and collateral requirements on letters of credit, potentially including taking a security interest in the contractor’s assets. Depending on the bank and the contract, these terms can be challenging for a contractor to fulfill. Surety bonds typically feature more flexible terms and, for contractors with credit problems, getting a surety bond with bad credit is often easier than getting a letter of credit.

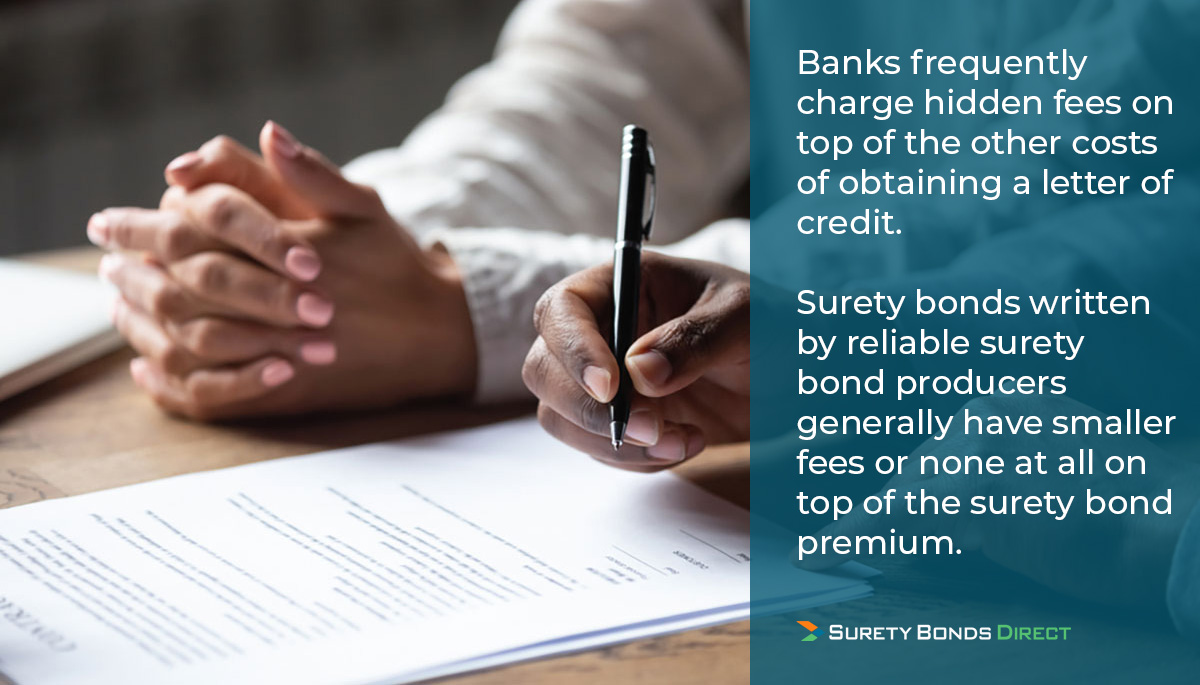

- Banks also frequently charge hidden fees on top of the other costs of obtaining a letter of credit. Surety bonds written by reliable surety bond producers generally have smaller fees or none at all on top of the surety bond premium.

- Surety bonds, as mentioned above, can be written to cover the entire duration of a project plus a maintenance period. Letters of credit have a fixed term of validity, which can mean an extra hassle to renew them when their term is up.

In some cases, a letter of credit may still be the appropriate choice, or a project owner may insist on a letter of credit rather than a surety bond. But for all of the above reasons, surety bonds are a smart choice for contractors.

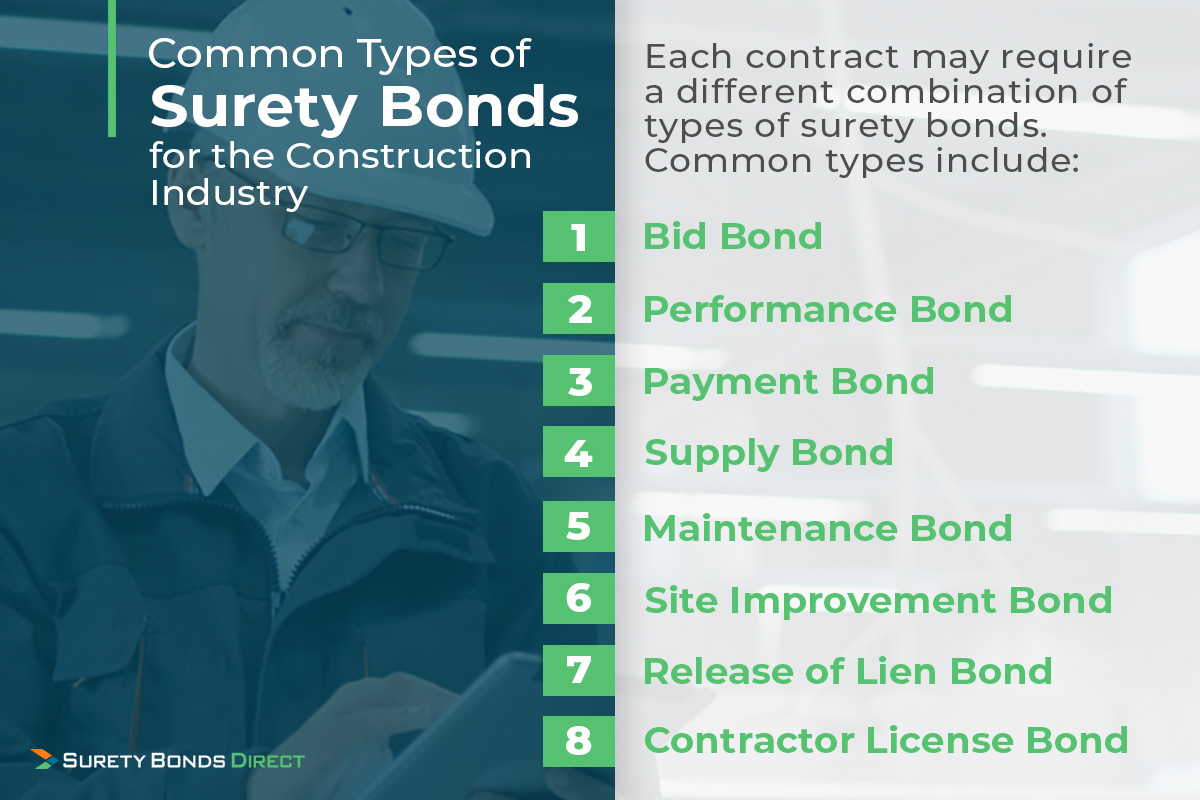

Common Types of Surety Bonds for the Construction Industry

Another advantage of surety bonds is that many different types of surety bonds are available to suit the needs of different contractors and projects. However, this also means that the principal needs to be aware of the major types of surety bonds that they may be required to obtain, including:

- Bid Bond: Guarantees that the contractor has the resources to complete the project as specified. A contractor must typically file a bid bond with the project owner as a part of the process for entering their bid. Almost all large construction projects, especially government projects, will require a bid bond.

- Performance Bond: Guarantees the contractor’s completion of the project to the specifications listed in the contract. A performance bond often provides funds to pay a new contractor to take over the project if the bonded contractor is unable to complete it or is removed from the project. The Miller Act requires that all federally funded construction projects valued over $100,000 be protected by both performance bonds and payment bonds (see below), and many state governments have enacted “Little Miller Acts” that impose similar requirements.

- Payment Bond: Guarantees the contractor’s payment of subcontractors and suppliers on time and in full. Typically, a contractor will purchase payment and performance bonds together in what’s known as a “P&P bond” package.

- Supply Bond: Guarantees the supplier’s delivery of all supplies and equipment. Unlike most other types of construction surety bonds, supply bonds protect the contractor from another party’s breach of contract.

- Maintenance Bond: Guarantees the contractor’s obligation to correct or financially compensate for any workmanship defects discovered after the fact.

- Site Improvement Bond: Guarantees the completion of a contract to improve an existing site or structure. A site improvement bond is similar to a performance bond but is specific to renovation and site improvement contracts.

- Release of Lien Bond: Guarantees that the owner of a property with a mechanic’s lien against it will pay the full amount owed on the lien. Release of lien bonds are used to allow the seller to sell the property while assuring lien holders that the property owner still intends to pay. This type of bond is used both in the construction industry and in other industries such as real estate.

- Contractor License Bond: Guarantees that a contractor will follow the law and conduct themselves according to the ethical standards of their state contractor licensing authority. Rather than being attached to a specific contract, this type of bond is attached to a contractor’s license. Most state and some city governments require that every contractor purchase and submit a contractor license bond before the government will issue a contractor’s license.

Each contract may require a different combination of types of surety bonds. However, the process of how to get a surety bond is broadly similar across different types.

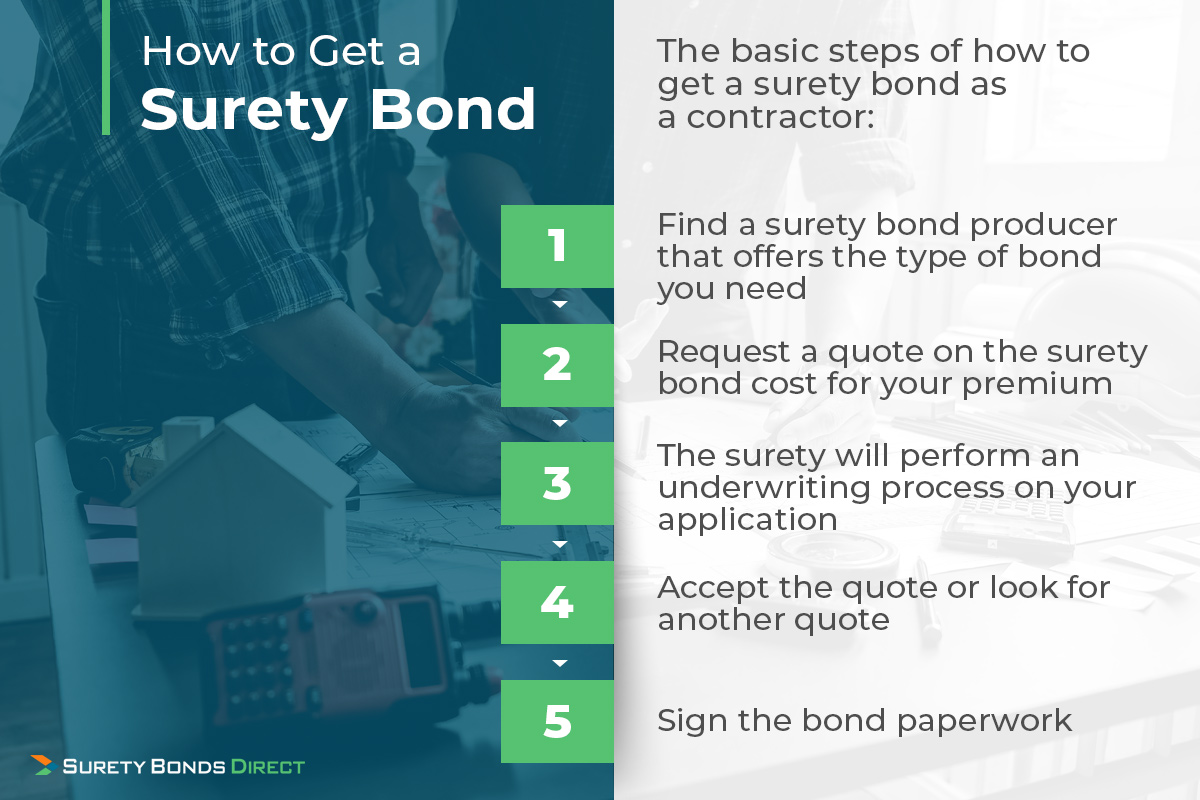

How to Get a Surety Bond

Another advantage of surety bonds is that the process for purchasing them is usually relatively simple. These are the basic steps of how to get a surety bond as a contractor:

- Find a surety bond producer that offers the type of surety bond that you need.

- Request a quote on the surety bond cost for your premium. You’ll need to provide some basic information about your business and credit history, as well as the value of the contract and any required penalty sum.

- The surety will perform an underwriting process on your application to assess your risk level. When underwriting is complete, the surety will email you a quote.

- You may either accept the quote and pay the premium or look for another quote. Once you’ve paid the premium, the surety will write the bond.

- The surety will send the bond paperwork to you for your signature. For many types of surety bonds, it’s possible to receive and sign the paperwork digitally. Once you’ve signed the bond paperwork, submit it to the obligee along with any other required materials.

Surety Bonds Direct is an industry leader in fast and easy surety bonding. Thanks to our wide network of highly rated sureties and our exclusive focus on surety bonds, we’re able to provide surety bonds at affordable premiums, even for principals with imperfect credit. When you’re ready to go direct, call us at 1-800-608-9950 or get a free quote online in just minutes.

updated: