Everything You Need to Know About the Surety Underwriting Process

What can you expect from the surety bond underwriting process, who are the surety bond parties, and how do the various elements of the process interact?

Surety bonds are a requirement for many different kinds of businesses. From car dealership bonds to contractor bonds, it’s important that businesses obtain a surety bond to guarantee their obligation to their clients and the federal, state or local government agency requiring the bond. As part of getting your surety bond, you’ll often need to go through the surety underwriting process.

What is underwriting and how will it affect your surety bond cost? What can you expect from the surety bond underwriting process, who are the surety bond parties, and how do the various elements of the process interact? Today, we’ll draw back the curtain on the surety underwriting process. We’ll give you a step-by-step guide to what goes on inside a surety underwriting department, how it can affect your surety bond premiums, and how to get a surety bond fast for an affordable price.

Surety Bond Parties

First, there’s a fundamental question to understand: What is a surety bond? Basically, a surety bond is a legally binding financial guarantee for a contract or obligation. Surety bonds are structured as an agreement between three parties. The surety bond parties are:

- Principal

- The party that applies for and obtains the surety bond (usually a business or individual)

- Obligee

- The party that requires the principal to obtain the surety bond (usually a government agency or project owner)

- Surety

- The neutral third party that provides the financial guarantee for the principal’s obligations

The surety always takes on a level of risk by writing a surety bond for a principal. To minimize this risk, the surety will typically use an underwriting process when deciding whether to issue a surety bond to a principal who has applied for one. The underwriting process also determines the rate category for the applicant and in turn, the price that the applicant will pay for the surety bond.

What Is Surety Underwriting?

Surety underwriting is the process that a surety uses to evaluate a principal’s risk level. The goals of the surety underwriting process are:

- To write surety bonds for principals who are less likely to have a claim filed against them

- To write surety bonds for principals who will pay the surety back if the surety does pay a claim

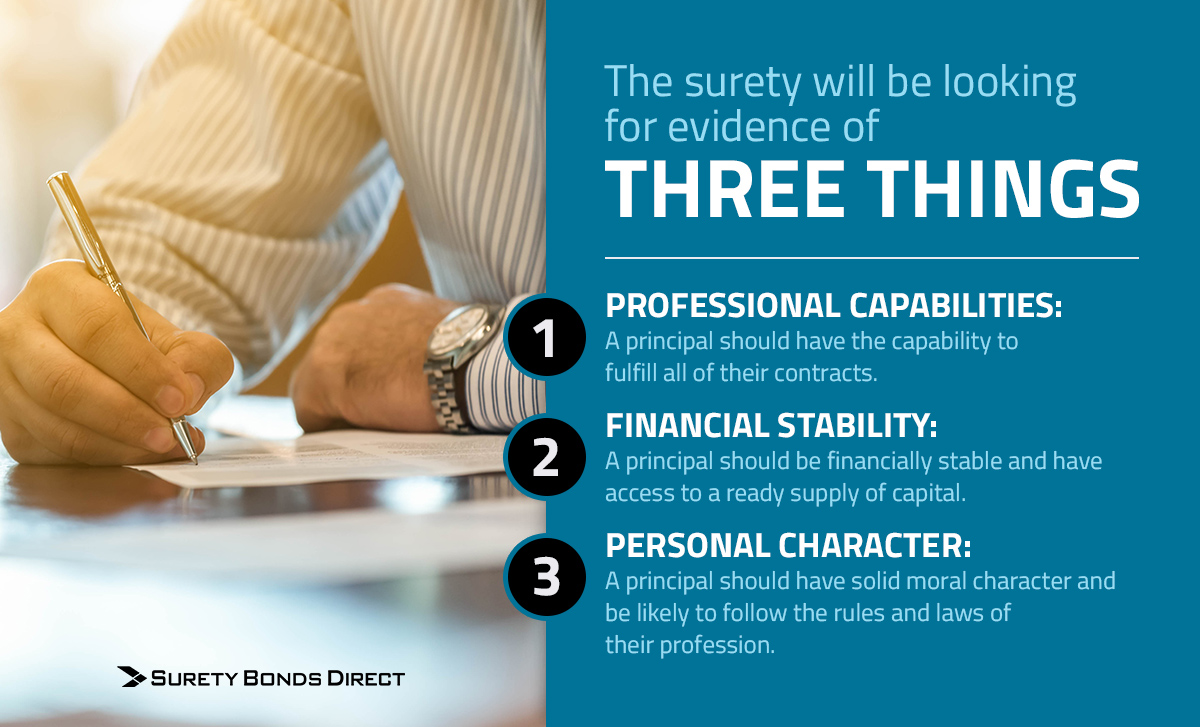

To achieve these goals, the surety will analyze the principal’s credit, financial position, and personal history in the underwriting process. The surety will be looking for evidence of three things:

- Professional Capabilities: A principal should have the capability to fulfill all of their contracts.

- Financial Stability: A principal should be financially stable and have access to a ready supply of capital.

- Personal Character: A principal should have solid moral character and be likely to follow the rules and laws of their profession.

How does a surety assess these characteristics in a principal? In the following sections, we’ll examine the process that sureties use to evaluate a principal’s risk level and the factors that surety underwriters look for. Before we dive in, though, it’s important to quickly clarify the difference between insurance underwriting and surety underwriting.

Insurance Underwriting vs. Surety Underwriting

Most people know that insurance companies also use underwriters to determine risk levels. Adding to the potential confusion, many states classify surety bonds as a form of insurance.

The key difference is that an insurance company expects claims to be made on its policies. Because insurance policies mostly cover circumstances out of the policy holder’s control, the insurance company includes an eventual expectation of a claim in its pricing model.

Most surety bonds never have a claim made against them, and the principal is ultimately responsible for paying the surety back for any money paid to a claimant. That means that a surety bond is more like a line of credit or an indemnification, so a surety doesn’t price the bond with much of an expectation of absorbing the financial impact of paying out a claim.

Because the principal must repay the surety for any claims, it’s critical to consider a surety bond as a binding financial obligation and to have contingencies in place for repaying the surety if a claim is filed. However, the best policy is always to follow the laws and ethical rules of your industry to prevent claims from being filed in the first place.

What Happens During the Surety Underwriting Process?

The surety bond underwriting process follows these steps:

- The principal applies for a surety bond through a surety company or surety bond broker.

- On the bond application, the principal provides information to the surety about their business and financial history.

- The surety performs a more detailed evaluation of the principal’s financial information and history.

- Based on the risk level that the underwriters determine, the surety provides the principal with a quote for a surety bond premium.

The process is relatively simple on the principal’s end. Behind the scenes, however, the surety’s underwriters are using a wide variety of factors to determine a principal’s risk level. Let’s look at what these factors are.

What Do Surety Underwriters Look For?

Surety underwriters look for anything in a principal’s personal and financial records that might indicate an elevated risk of surety bond claims. This can include:

- Low credit score

- Having declared bankruptcy

- Felony convictions

- Lack of relevant experience

- Large amounts of debt

- Previous surety bond claims against the principal

- Previous license revocations, suspensions, or disciplinary actions against the principal

- Lawsuits against the principal

- Tax liens against the principal

Any of the above factors will raise a principal’s surety bond premiums, but credit score is particularly important for the surety bond underwriting process. Remember that a surety bond is similar to a line of credit. Thus, any credit factors that would make it more difficult to get a loan or a credit card will also usually increase surety bond premiums.

The surety will also examine the terms of the bond required during the underwriting process. For a surety’s underwriters, any of the following surety bond characteristics will increase the risk level of bonding a principal:

- Types of surety bond that frequently have claims filed against them

- Surety bonds with a large penalty sum

- Surety bonds with multi-year terms

- Language that leaves the surety liable for an amount larger than the penalty sum

Once they’ve assessed the principal’s history and the terms of the bond, the surety’s underwriters will determine a premium based on the risk factors listed above and send the principal a quote. Although surety underwriters don’t provide the exact methodology that they use to weigh each factor, they use a combination of old-fashioned investigative diligence and advanced “insurtech” innovations that allow them to automatically rate various factors using big data and algorithms.

How Much Does a Surety Bond Cost?

When a principal purchases a surety bond, they usually don’t pay the full amount of the penalty sum. (The exception is certain types of court bonds.) Instead, the principal pays a percentage of the penalty sum as a premium. The premium system helps principals meet their surety bond obligations while preventing them from having to tie up large amounts of capital in a surety bond.

A principal with good credit and financial history can usually expect to pay around one to three percent of the coverage amount. However, principals with lower credit scores or other risk factors will often face higher premiums.

Once the principal receives their premium quote from the surety, the principal may then choose any of the following options:

- Accept the quote and purchase the surety bond.

- Shop around for a quote from a different surety or surety bond broker.

- Work with the surety to find ways to make the premium more affordable. In some cases, a co-signer or collateral deposit arrangement can be used to bring down the premium.

The last option is particularly important for principals who may be facing higher premiums due to a lower credit score or other factors. Let’s look at how you can do it.

How Can I Lower My Surety Bond Premiums?

The good news is that even if your underwriting process results in a higher premium, there are still ways to get a surety bond fast and for an affordable price. Here are some options that Surety Bonds Direct offers:

- Working with Specialists: Many sureties specialize in bonding principals with low credit for an affordable premium. We work with a wide network of sureties who are willing and able to bond principals with lower credit scores.

- Adding a Co-signer: Principals can often lower their surety bond cost by adding a co-signer to their bond. A co-signer is typically a spouse, relative, or business partner who becomes jointly financially responsible for the bond with the principal. You’ll want to choose a co-signer with good credit, as the surety will evaluate your creditworthiness on the basis of the combined credit of you and your co-signer.

- Using Premium Financing: Surety Bonds Direct offers surety bond premium financing options that allow you to spread your premium payments out over time and get your surety bond now. Just ask our bond specialists if your bond premium qualifies for financing.

To learn more, see our resources on how to get a surety bond with bad credit. A lower credit score shouldn’t keep you from opening a business or entering a new profession, and Surety Bonds Direct can help you navigate the surety underwriting process to find a more affordable premium.

Surety Bonds Without Underwriting

Not all types of surety bonds require an underwriting process. Sureties consider many kinds of bonds, such as vehicle title bonds, certain contractor license bonds, notary public bonds and public insurance adjuster bonds, to be low-risk due to their relatively low number of claims and/or small penalty sums. Principals can purchase these “pre-approved” surety bonds instantly online from Surety Bonds Direct for a flat fee, with no underwriting process necessary.

Simply enter your basic information, including the state your business is located in and name as it will appear on the bond, pay the premium, and Surety Bonds Direct will send you your surety bond approval instantly. In these cases, you will receive your official surety bond instantly or via email usually on the same day. Note, however, that like most other surety bonds, these instant surety bonds must still be renewed periodically (often on an annual basis).

Renewing Your Surety Bond

Most surety bonds remain in force for a period of time determined by the type of bond or by the obligee. Some surety bonds, such as construction bid bonds, are released upon completion of a project. Many others must remain in force for as long as a business continues to operate.

It’s important to know that when you renew your surety bond, you’ll need to undergo a new surety underwriting process. In most cases, this will be a straightforward process, and you’ll pay approximately the same premium that you did before.

However, if your financial situation has changed dramatically, your business has been sued, a claim or complaint has been filed against you, or any other underwriting factor has changed, your premiums may be different. If your premiums increase when renewing your surety bond, consider one of the previously mentioned strategies for lowering your surety bond premiums.

Do you have more questions about the surety bond underwriting process, surety bond parties, or anything else we’ve discussed here? Our surety bond experts will be happy to help. Call us anytime at 1-800-608-9950 or get your free and fast surety bond quote online today.

updated: