Surety is Different than Insurance

Surety works differently than almost all other insurance products. Be an informed consumer and learn the differences.

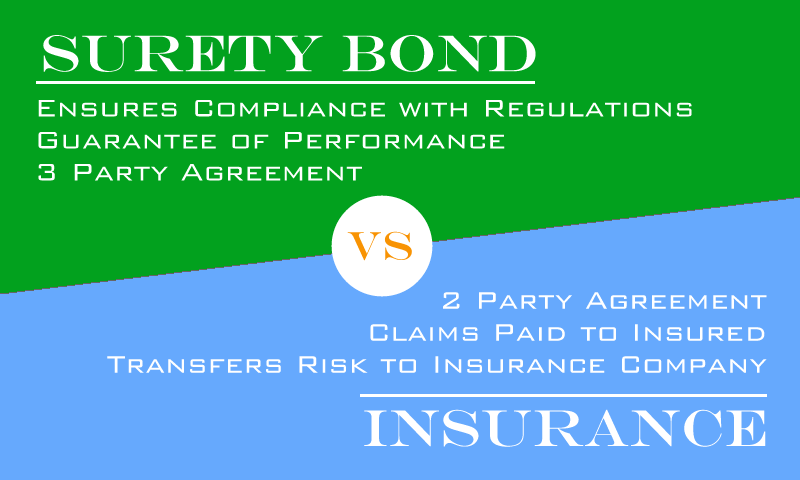

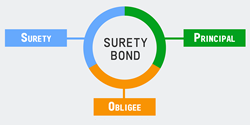

The most basic difference between surety and insurance is that surety is a three party arrangement and insurance is a two party arrangement. Unlike most types of insurance a surety bond is required by, and protects the interest of, this third party (obligee) rather than the insured. Therefore, surety bonds are usually purchased not for one's own sake but as a requirement of a third party (e.g. a municipality, state, federal government, court or construction project owner). Also check out our article What is a Surety Bond?

Watch our video explaining the difference between a surety bond and insurance.

Who does a surety bond protect?

With traditional insurance, the risk of loss is transferred to the insurance company but in surety, the risk remains with the principal. For example, your auto insurance company will pay you for damages to your car in the event of an accident. In contrast, your surety company will pay your customer if you violate the terms of your surety bond. Furthermore, you may be ultimately responsible reimbursing your customer for the financial loss. This risk transfer in surety is handled through an indemnity clause that is signed by the applicant as part of the bond application.

How does a surety bond work?

Another surety insurance difference is that surety works more like a credit product than an insurance product. Traditional insurance risks are evaluated based on the possibility of a loss happening to the insured considering how often similar losses have occurred in the past under like conditions (e.g. the probability of a hurricane damaging a home along the Florida coastline). Whether the homeowner has a credit score of 750 or 500 is probably irrelevant to the risk of loss.

On the other hand, similar to a loan, surety risks are more about the creditworthiness and character of the bonded (insured) because damages typically arise directly from the actions of the bonded (e.g. failure to pay taxes, unethical business practices, non-compliance with codes, or misrepresentation). In this case, surety companies do believe the auto dealer with a 750 credit score presents a lower risk of loss than one with a 550 credit score. This is why surety underwriters rely heavily on credit score as the key factor in evaluating applicants for most bonds.

What is surety insurance?

Surety bonds are often times referred to as "surety insurance", "surety bond insurance" or "insurance bonds". This is usually because surety bonds are regulated in most states as a form of insurance even though as discussed above, surety is very different from insurance. Surety bond requirements also get grouped with insurance requirements in the licensing process in many states. The surety insurance term is also used sometimes to describe situations where a surety bond may be purchased in lieu of insurance.

What does cash or surety mean?

Cash or surety bond usually means that there are two options to meet the financial or indemnity requirement. Cash may be deposited with the requiring party and the money is held in reserve until the obligation is satisfied.

Alternatively, a surety bond may be purchased and posted for the benefit of the requiring party. Often times a surety bond is the preferred method because surety bond costs are a percentage of the bond amount so they do not require so much cash up front. For example, a bond applicant may be more comfortable meeting a $100,000 security requirement by paying a $1,000 premium annually (1% of the bond amount) to a surety company for a bond versus depositing the full $100,000 with the obligee.

updated: