Ask yourself these two questions and you'll likely find the exact type of surety bond you need so you can get pricing and get this process done.

Question 1 - Who's Asking For The Surety Bond?

As a small business, you're likely being asked (or required) to purchase this surety bond.

And as a small business, there are primarily only two types of surety bonds that are a hard requirement:

- License surety bonds

- Tax surety bonds

License Surety Bonds

If you're applying for a license so you can perform a job like...

- Electrician

- Concrete installer

- Insurance adjuster

- Auto dealership

- Mortgage broker

You need a license based surety bond so to find yours search for your industry plus surety bond. The above jobs would correspond with the following bonds:

- Contractor license bond (both electrician and concrete installer)

- Insurance adjuster bond

- Vehicle license bond

- Mortgage license bond

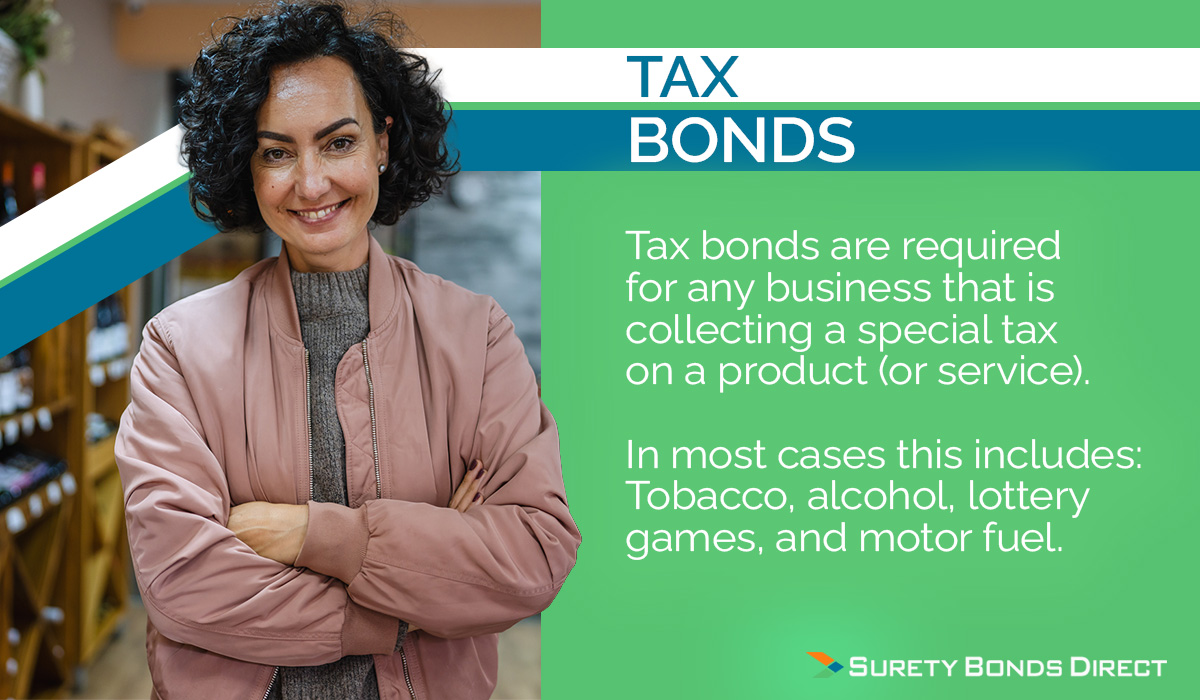

Tax Bonds

If you're collecting a specialized tax when selling your product, which can include:

- Tobacco tax

- Alcohol tax

- Lottery games tax

- Fuel tax

In this case you need a tax surety bond. This can get a little more complicated to find the right one but in the majority of cases, search for the type of tax you're required to pay.

Examples can include:

Examples of tax bonds that are more specialized include:

Other Possible Bonds

There are a few other bonds that a small business may need.

If you're a contracting business and you're bidding on projects, you'll need one or more of the following construction based surety bonds:

If you're a dealership who operates in the used vehicle market or maybe your business purchased a used delivery truck...

You might need a vehicle title bond so you can get a vehicle titled in your state.

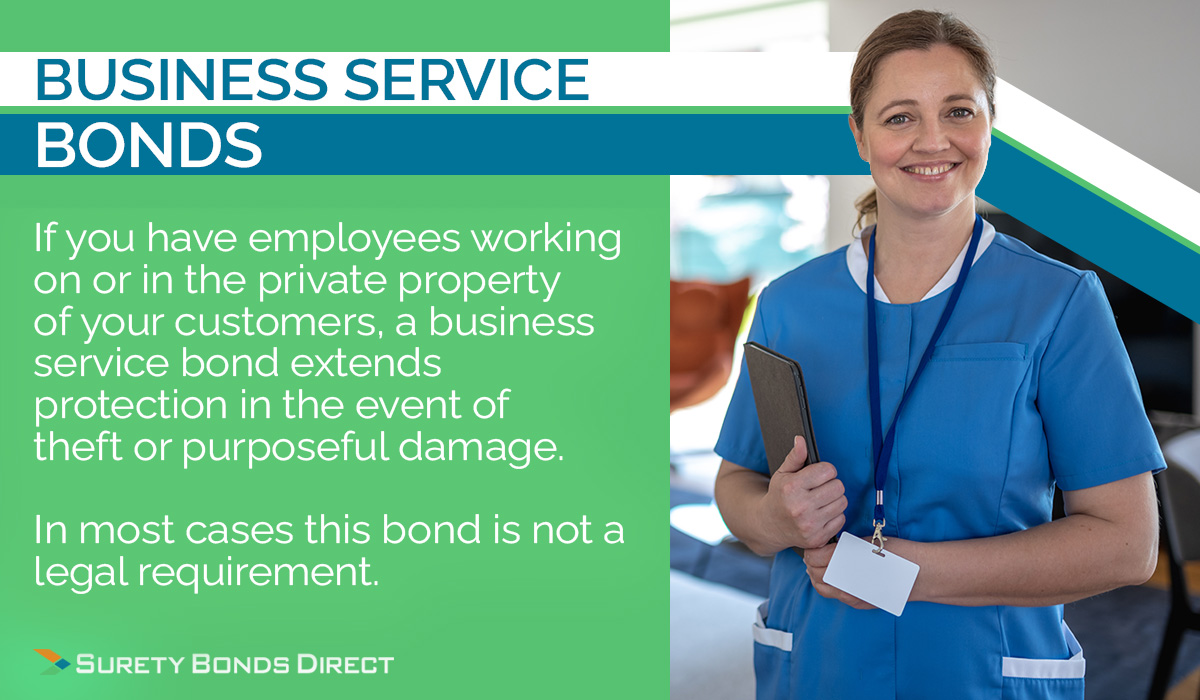

Question 2 - Does Your Business Operate On Or In Your Customers Private Property?

Business Service Bonds

A lot of small businesses provided their service by having the owners and/or employees work on or in the private property of their customers. Examples can include:

- Home services contractors

- Home cleaning companies

- Commercial janitorial companies

- Home health care services companies

- Landscaping companies

For many businesses that operate on or in private property it can make a lot of sense to purchase a business service bond.

A business service bond is - in most cases - not a hard requirement to get a job or land a project.

However, it's a great marketing tool that allows your business to say, "We are bonded."

Being bonded with a business service bond separates your business from the competition and indicates to potential customers that you have full trust in your employees.

You have so much trust that to put your customers worries to bed, you'll guarantee they will not steal or purposefully damage your customers property. If they do, the customer can make a claim for the financial damages against the business service bond.

Employee Dishonesty Bonds

This is a rare surety bond a business owner may elect to purchase. It's called an employee dishonesty bond and it's the only surety bond purchased by a business owner for the protection of the business owner.

If you have employees that handle valuable items or data, examples can include:

- Large sums of money

- Valuable intellectual data

You as the business owner can purchase this surety bond in the event that an employee steals for your business.

Read more about this unique employee dishonesty bond here.

Find The Right Surety Bond And Get Pricing With No Purchase Obligation

Now you should have some clear direction about how to find the correct surety bond for your small business.

To recap:

- If you've been asked to get a surety bond it's most like a license bond or a tax bond

- If you're choosing to purchase this bond it's most likely a business service bond

Click here and you search for the bond you need.

If this post helped you find the bond you need, click here and request pricing.

Call 1-800-608-9950 and you can talk with a bond specialist if none of the above cases matches your situation.

When you request pricing, you are not obligating yourself to purchase. It's our job to find you the lowest pricing and either we succeed and then you can decide if you want to buy, or we fail and you can go somewhere else.

So there's no risk to request pricing and get the information you need today to take the next step.